STRONG FINISH TO THE YEAR

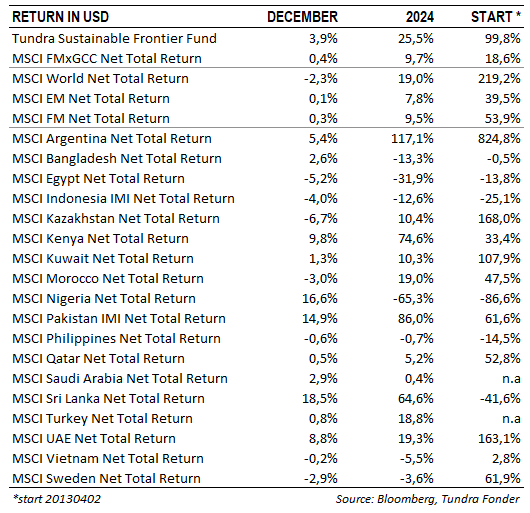

In USD the fund increased by 3.9% (EUR: +5.4%) in December, compared to the MSCI FMxGCC Net TR (USD) index, which rose by 0.4% (EUR: +1.8%), and the MSCI EM Net TR (USD) index, which increased by 0.1% (EUR: +1.5%).

In absolute terms (USD), Pakistan (+2.2% portfolio contribution), Sri Lanka (+1.1%), and Egypt (+0.7%) made positive contributions, while Kazakhstan (-0.3%) was the only individual market to contribute negatively. Relative to the index (USD), the primary contributors were our overweight positions in Pakistan (+1.5% relative portfolio contribution), Sri Lanka (+0.9%), and Egypt (+0.7%). The lack of holdings in Kenya (-0.3%) and Romania (-0.1%) negatively affected the relative return of the fund.

For the third consecutive month, the largest single contribution came from the Pakistani IT company Systems Ltd (9% of the portfolio), which gained an additional 10% amid a continued strong Pakistani market. As anticipated, local institutions have started shifting capital from the bond market to the equity market, driven by declining interest rates—a key factor behind Pakistan’s strong performance this year. The second-largest contribution came from Egypt’s GB Corp (5% of the portfolio), which rose 16% after a strong nine-month report. The most significant negative contribution came from the National Bank of Pakistan (5% of the portfolio), which fell 8% due to rumours of further provisions in the recently concluded pension case (see the September newsletter), as well as Kazakhstan’s fintech company Kaspi (3% of the portfolio), which dropped 10% without any notable specific events.

SUMMARY OF 2024

The strong year-end performance made 2024 the fund’s second-best since inception. In USD the fund rose 25.5% (EUR: +33.4%) compared to MSCI FMxGCC Net TR (USD), which gained 9.7% (EUR: +16.6%), and MSCI EM Net TR (USD), which increased by 7.8% (EUR: +14.6%). This marks the ninth year out of twelve in which the fund has outperformed the index. Since inception, the fund has risen 100% (EUR: +146%), compared to MSCI FMxGCC Net TR (USD) at 19% (EUR: +46%) and MSCI EM Net TR (USD) at 40% (EUR: +72%).

In absolute terms (USD), Pakistan (+14% portfolio contribution), Vietnam (+12%), and Sri Lanka (+4%) were the primary positive contributors, while Nigeria (-1.8%), and Indonesia (-0.8%) were the main detractors in 2024. Relative to the index, Vietnam was the strongest contributor (+14% relative portfolio contribution), driven by exceptional stock selection. Our Vietnam sub-portfolio increased by 49%, in a flat Vietnamese market. Pakistan contributed nearly as much (+11%) as our sub-portfolio rose 68%, compared to the market’s 86% increase. The third-largest relative contribution (+5%) came from Sri Lanka, where our sub-portfolio rose 53%, compared to the market’s 65%. This year, we were unable to fully keep pace with the respective markets in Pakistan and Sri Lanka during the risk-on environment. Looking at a five-year period from the end of 2019 (just before COVID-19), our Pakistani sub-portfolio has now increased by over 196%, compared to MSCI Pakistan IMI Net TR (USD), which rose 48% during the same period. Over five years, our Sri Lankan sub-portfolio has risen by 27%, compared to MSCI Sri Lanka IMI Net TR (USD), which fell by 28% during the same period. The key for us will always be the potential long-term absolute returns of our portfolio companies. This strategy has served us well since inception, both from an absolute and relative perspective.

OUTLOOK FOR 2025

As we move into 2025, risks are always present, so let us begin by addressing them.

In last month’s newsletter, we shared our expectations regarding how the U.S. under Trump might act, predictions with a high degree of uncertainty. This could create a challenging international business environment, with potential conflicts between the U.S., China, and Europe affecting global equity risk appetite. Even Vietnam, one of our key markets, might feel the impact, as it currently holds the world’s third-largest trade surplus with the U.S.

Another area closely linked to heightened geopolitical risks during the Trump era is the global interest rate environment. Our view remains that global interest rates will decline, but not to the near-zero levels seen in Europe and the U.S. between 2009 and 2022. However, in 2024, particularly toward the end of the year, we observed rising expectations for slower/lesser interest rate cuts in the U.S., the world’s largest market. This has had a clear impact, primarily on emerging markets with stronger economic ties to the U.S., such as Mexico and Brazil. Higher U.S. interest rates will also influence general interest rate levels in smaller, less developed emerging markets. There is now an increased risk of disappointment regarding where the interest rate cycle will bottom out.

Additionally, we must highlight the risk posed by the U.S. equity market, which has served as the engine for global equities over the past decade and now accounts for an astonishing 74% of the MSCI World index. Valuations are high, yet the U.S. stock market has consistently defied skeptics year after year. While we avoid predicting market crashes, investors should be aware that the exceptional performance of the U.S. stock market over the last decade is highly unusual. A significant negative movement in the U.S. would have a severe impact on global equity portfolios and dampen global risk appetite. We often say that smaller emerging markets tend to thrive in a stable global environment, particularly when stock markets in the U.S. and Europe exhibit moderate and steady performance within a +/-10% range.

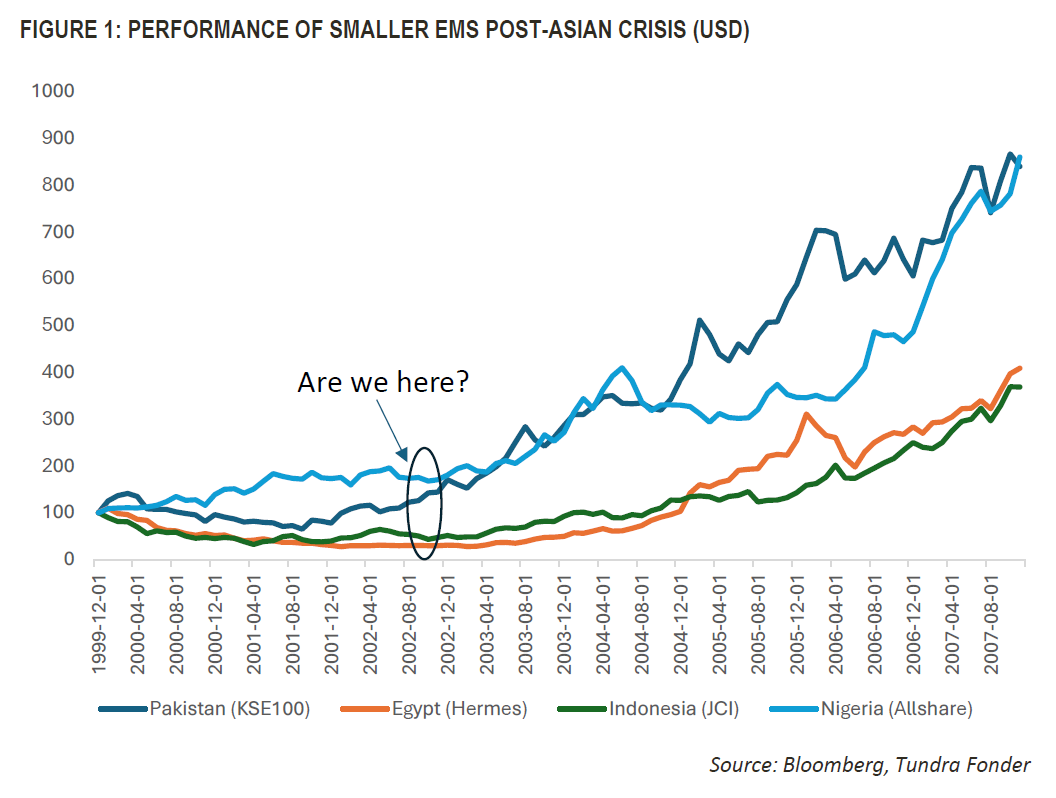

External risk factors could, therefore, affect all equity markets. However, when we focus on each of our core markets, we must acknowledge that visibility has rarely been this clear. This may not be surprising, given that we have just emerged from the worst crisis in 30 years. Crises like the Asian and Ruble crises of 1997–1998 are often followed by several strong years. Given the severity of this recent crisis, it points to a longer period of positive development. Even if the same mistakes eventually resurface—such as futile attempts to manage currency values—the resulting imbalances take time to build. In the best-case scenario, our most affected countries have learned valuable lessons from their experiences in recent years. For example, we do not anticipate Sri Lanka engaging in aggressive foreign currency borrowing in the near future. Similarly, we see clear signs of significant import substitution in Pakistan, particularly in the energy sector, along with emerging export opportunities across different sectors.

Regardless of whether these countries have fully learned from past mistakes, we believe the next 3–4 years could be a more favorable period for Tundra’s markets. Our focus will remain on consistently delivering superior returns in each of the markets in which we invest.

REAFFIRMING TUNDRA’S INVESTMENT PHILOSOPHY

2024 was a strong year, but it followed a couple of less remarkable years.

Tundra distinguishes itself in the frontier market category through its thematic focus on low-income and lower-middle-income countries, often including significant exposure to markets that many investors deem uninvestable. Those familiar with our approach will recognize that our primary focus has always been on the development and valuation of individual portfolio companies, rather than being influenced by media narratives about a country’s challenges or the reactions such narratives may provoke in other investors (selling due to increasing fear). It is essential to differentiate between a country’s macroeconomic or political problems and the actual impact on its listed companies. Our focus has always been on identifying well-managed businesses whose operations are strategically aligned with their country’s long-term opportunities and challenges, enabling them to perform effectively in both favorable and adverse conditions, thereby generating absolute returns over several cycles. Confidence in a portfolio company’s resilience and long-term potential is particularly critical during challenging periods. Thorough company analysis—rather than relying on courage, which has no place in fund management—is key to achieving strong long-term returns. When investor sentiment shifts, rebalancing often happens rapidly, underscoring the importance of contrarian thinking, trusting one’s decisions, and maintaining patience to reap the eventual rewards. Pakistan and Sri Lanka serve as two timely examples of this approach in action.

Tundra’s definition of frontier markets encompasses low-income and lower-middle-income countries—a group that currently accounts for 50% of the world’s population and is projected to rise to 67% in the next 50 years. This group is also the only one in the world where the working-age population (15–64 years) will continue to grow over the coming decades. As a result, generic economic activities, such as building roads, hospitals, and schools, will remain higher in these countries in the foreseeable future. However, we are the first to acknowledge that high levels of economic activity do not necessarily translate into strong stock market performance. On average, the quality of companies in these markets is lower compared to countries like Sweden or the United States. Therefore, we place a significant emphasis on stock-picking, with parts of our investment team based in some of our key investment countries, and our portfolio managers spending a substantial portion of the year traveling.

Given that per capita carbon emissions in these countries are currently about one-tenth of the level in the world’s wealthiest nations, this part of the world will have the most significant impact on shaping the planet’s environment in the coming decades. Their businesses will face increasing regulations as their economic and environmental footprints grow. However, the most fundamental aspect of our sustainability work is aligned with the UN’s Goal #1: Eradicating poverty. Before families have food on the table, children can attend school, and the lights at their study desks are on, it is difficult to focus on activities like recycling plastic bags. As foreign observers, it is easy to compare these nations to developed countries, but one must understand that these countries are far behind in terms of economic development. They are early in their sustainability journey and our analysis must account for this.

Our sustainability efforts, therefore, primarily focus on ensuring we invest in companies with honest owners and skilled management teams operating in future-oriented sectors. Good companies understand the importance of how environmental considerations and worker treatment influence their potential for continued growth. Many investors associate sustainability with charity, i e sacrificing returns for the greater good. This is a common misconception. In our view, only competitive companies led by competent businesspeople can contribute to a better society in the long run. We thus see no conflict between long-term sustainability efforts and long-term business success. Competent business leaders understand the necessity of building their operations in a sustainable manner. These are the companies we invest in, and we are there to support them in their long-term growth journey.

___________________________________

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you will be able to recover all of your investment. Historical return is no guarantee of future return. The Full Prospectus, KIID etc. are available on our homepage. You can also contact us to receive the documents free of charge. Please contact us if you require any further information: +46 8-5511 4570.