BREATHER AFTER SEVERAL STRONG MONTHS

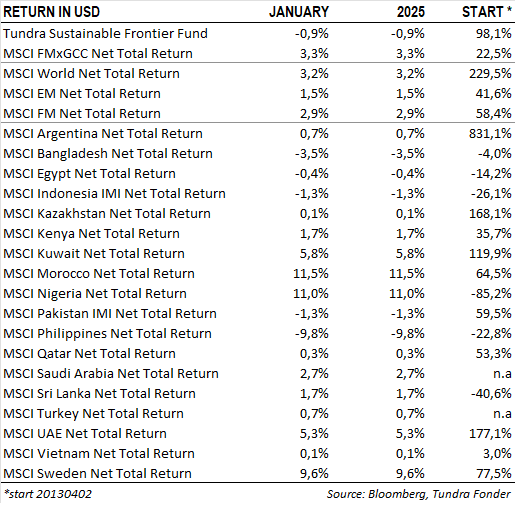

In USD the fund declined by 0.9% (EUR: -0.5%) in January, compared to the MSCI FMxGCC Net TR (USD), which rose by 3.3% (EUR: +3.7%), and the MSCI EM Net TR (USD), which increased by 1.5% (EUR: 1.9%). In absolute terms, Morocco (+0.4% portfolio contribution), along with Egypt (+0.4%), Nigeria (+0.3%), and Sri Lanka (+0.3%), contributed positively, while the Philippines (-1.1%), Indonesia (-0.6%), and Pakistan (-0.5%) were the markets that detracted the most. Relative to the index, our overweight positions in Egypt (+0.4% relative portfolio contribution), Nigeria (+0.3%), and Sri Lanka (+0.3%) provided positive relative returns during the month, while our overweight in the Philippines (-1.1%), underweight in Morocco (-1.1%), underweight in Slovenia (-0.9%), and overweight in Indonesia (-0.6%) were the largest detractors.

The strongest individual contribution came from Moroccan payments company Hightech Payments (2.5% of the portfolio), which rose by 18% in a robust Moroccan stock market. The second-largest individual contributor was Pakistan’s National Bank of Pakistan (5% of the portfolio), which rose by 8%. The rise came after speculation emerged that the company might resume its dividend, a theory we share. The largest negative contribution came from Indonesian healthcare company Hermina Hospitals (3% of the portfolio), which fell by 15% during the month as the company slightly adjusted their margin guidance downwards for the full year. The second-largest negative contribution came from Century Pacific (4% of the fund), which dropped by 13% without any specific corporate events.

KEY NEWS

Emerging markets experienced turbulence as Trump appeared to proceed with his threat to impose tariffs on both Mexico and Canada. A compromise was reached just before the tariffs were due to take effect, leading to a market rebound. This aligns with our theory that Trump primarily uses tariff threats as a negotiating tool in his international relations. However, caution is advised in assuming that his administration’s actions will always be based on rational economic reasoning. Trump (at least temporarily) proceeded with the imposition of 10% import tariffs on Chinese goods. The US imports over USD 400 billion annually from China, representing approximately 15% of total US imports. China responded immediately by imposing equivalent tariffs on USD 14 billion worth of US imports (out of a total of approximately USD 160 billion). Additionally, China launched an antitrust investigation into Google and imposed restrictions on the export of certain critical minerals to the US. Negotiations are reportedly ongoing, and it remains to be seen whether this issue will also be resolved through diplomacy. There is market concern that Europe could be the next target for such “negotiations”.

In January, the State Bank of Pakistan (SBP), the country’s central bank, cut its policy rate by another 100 basis points to 12%, in line with market expectations. Since the summer of 2024, the central bank has reduced its policy rate by a total of 10 percentage points. This monetary easing was supported by a disinflationary trend, with January’s CPI recorded at 2.4%, the lowest level in nine years, primarily due to base effects. Our base scenario is that inflation will gradually rise to 8–9% by the summer of 2025, as favourable base effects dissipate. This suggests that Pakistan’s monetary easing cycle is nearing its end. In its monetary policy report, the central bank revised its inflation and current account forecasts for the 2025 fiscal year while maintaining its GDP growth forecast. The bank now expects inflation to range between 5.5% and 7.5%, a significant revision from the previous estimate of 11.5% to 13.5% at the start of the fiscal year. Similarly, the current account balance is now projected to be between +0.5% and -0.5% of GDP, compared to the earlier forecast of 0% to -1.0% of GDP. At the same time, the central bank has maintained its GDP growth projection of 2.5% to 3.5%. We note that both the pace of rate cuts and the decline in inflation have so far been faster than we had anticipated. Additionally, the current account balance has been unexpectedly strong, allowing the central bank to make net foreign exchange purchases. While we maintain our base case for monetary policy, we acknowledge room for positive surprises. The stock market is now trading at approximately 6.0x on 2025 earnings, compared to the ten-year average of around 8.0x. The sharp decline in interest rates since the summer of 2024 initiated some buying from local institutions during the autumn, but volumes have been relatively modest, and since the beginning of the year, both local equity funds and foreign investors have been net sellers. The market has been consolidating since mid-November, but we believe that the rate decline observed so far has not yet been fully priced in. Provided there are no unexpected political developments or complications arise in discussions with the IMF we estimate that there is still a significant distance to go before earnings growth and reform ambitions become the primary driving factors.

COMPANY-SPECIFIC NEWS

Square Pharmaceuticals published its results for the October–December period. Despite a challenging environment for the pharmaceutical sector, where drug prices are regulated and have yet to be adjusted to compensate for rising costs, the company reported strong earnings growth. In Q2 of the 2025 fiscal year, Square Pharma posted revenue growth of 12.6%, driven by double-digit growth in both the domestic market and export sales. However, operating profit growth lagged at 8.1% year-on-year due to increasing cost pressures. Nevertheless, the company reported net profit growth of 25.9% year-on-year, primarily due to a substantial increase in financial income on its USD 467 million cash balance and higher dividend income from its associated companies. Square Pharma is currently trading at just under 9.0x of annual earnings, compared to its ten-year average of 15.1x. In terms of P/B, the company is valued at 1.5x, which is roughly half its ten-year average.

Our Pakistani portfolio holding, Airlink, the country’s largest assembler and distributor of mobile phones, officially announced the launch of smart TVs in partnership with Xiaomi, marking its entry into a market valued at over USD 160 million, with an annual demand of approximately 0.9 million units. Leveraging its expertise in mobile assembly and distribution, Airlink aims to establish a market-leading position in smart TVs by capitalising on Xiaomi’s strong brand equity and technology. Additionally, Airlink announced the acquisition of additional land in an economic zone that offers a ten-year tax holiday. The company plans to shift a significant portion of its production from its existing facility to the new plant, which is expected to reduce its effective tax rate and enhance earnings by at least 20% compared to previous estimates. Beyond business expansion, Airlink is playing a crucial role in technology transfer through its partnerships with global brands while also benefiting from Pakistan’s competitive labour costs to create employment opportunities for the country’s youth. As Pakistan formulates a mobile device manufacturing and export policy, any favourable developments in this regard could unlock substantial export earnings and job creation. We believe Airlink is well-positioned to be at the forefront of this opportunity.

___________________________________

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you will be able to recover all of your investment. Historical return is no guarantee of future return. The Full Prospectus, KIID etc. are available on our homepage. You can also contact us to receive the documents free of charge. Please contact us if you require any further information: +46 8-5511 4570.