VIETNAM AND PAKISTAN LED THE WAY DURING MAY

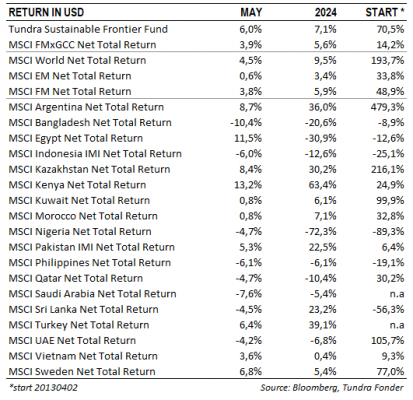

In USD, the fund rose 6.0% (EUR: +4.4%) during the month of May, compared to MSCI FMxGCC Net TR (USD), which rose 3.9% (EUR: +2.4%), and MSCI EM Net TR (USD), which rose 0.6% (EUR: -0.9%). In absolute return, it was primarily Vietnam (+3.6% portfolio contribution) and Pakistan (+2.8% portfolio contribution) that contributed positively, while it was mainly Bangladesh (-0.6% portfolio contribution) and Sri Lanka (-0.1% portfolio contribution) which reduced the absolute return. Relative to the benchmark index, it was again Vietnam that primarily contributed to the outperformance in the month. Our sub-portfolio rose 14% during the month compared to the market, which rose 4%.

On holding level, the biggest single contribution came from the fund’s largest Pakistani position, Systems Ltd (7% of the portfolio), which rose 18%. The stock has been out of focus in Pakistan during a period when it was primarily the hardest hit sectors during the crisis that recovered. The company’s position as a net exporter, and thus a beneficiary of a weaker rupee, has been negative during a period when the Pakistani rupee has strengthened. In addition, the company is making a major expansion in the Middle East, which has hurt margins in the short term. We had the opportunity to speak with the company’s CEO, Mr. Asif Peer, at an investor conference at the end of May and we have rarely heard him more positive about the immediate future. Among individual holdings, the Vietnamese airport operator Airports Corporation of Vietnam (4% of the portfolio) also stood out. The stock rose 24% in a slow local equity market. Stronger-than-expected international traffic, including the previously subdued Chinese market, was the primary reason for the rise. It now looks like 2024 could be the first year in which international traffic exceeds the pre-covid year 2019.

IMPRESSIONS FROM OUR TRIP TO SRI LANKA

During the month, we visited Sri Lanka, where we met some of our portfolio companies, and also had the opportunity to visit important infrastructure projects.

Sri Lanka has five tough years behind it. The problems started in 2019 when a coordinated terrorist attack in the spring led to a dramatic decline in the important tourism revenue (previously 5-6% of GDP and growing). This was followed by COVID which completely shut down tourism for two years. Lack of crucial tourism revenue in combination with excessive borrowing in foreign currency, the country ended up in problems. The government, led by the Rajapaksa brothers, gambled on a quick recovery and tried to stimulate itself out of the debt trap by cutting taxes while imposing capital controls. When Russia invaded Ukraine and commodity prices skyrocketed, the situation became unsustainable. The country was forced to suspend payments on its foreign currency-denominated debt and devalue its currency. In 2022, the country’s GDP decreased by 10% and its foreign reserves were down to basically zero. The lack of foreign currency meant even essential products, such as fuel and medicines, could not be imported, which created widespread social unrest. Under the country’s new president, Mr. Wickremasinghe, an agreement has been concluded with the IMF, and negotiations with the creditors have come a long way. The tourists have returned, and the 2024 visitor numbers will end up close to 2018 (the year before the terrorist attack). The crisis of the past five years is still fresh in the minds of locals, though, and even if one anticipates optimism, it is still subdued. In the World Bank’s presentation, they spoke of a “normal” growth of between 2-4% provided that a continued sensible economic policy is pursued, and up to 6% if more aggressive reforms are implemented. The IMF agreement follows a restrictive financial policy with a need for higher tax revenues and to preserve the confidence of investors, the central bank will probably have to be cautious in its actions. A presidential election awaits in the fall, where currently a clear left-wing candidate is leading in the opinion polls. Even if the consensus in the market is that the IMF agreement will be adhered to regardless of the candidate, it creates uncertainty in the market and causes corporates to adopt some caution in their investment plans. The currency devaluation and subsequent new agreement with the IMF coupled with the debt restructuring have given Sri Lanka breathing space and a new base to build from. It has also given the country a chance to regain its natural competitive advantages in tourism and services. We noted with interest the increasingly strong economic ties with India, where the port of Colombo today mainly handles Indian imports and exports, and leading Indian companies have announced investments in the hotel industry as well as in renewable energy. We are likely to see more similar announcements in the years to come. Assuming no major departures from the current economic plan, the country should be able to post a current account surplus going forward that is sufficient to handle its remaining repayments of the foreign debts built up mainly in 2012-2019 and still be able to continue its journey towards becoming an upper middle-income economy like its peers in emerging markets.

On our trip, we met some of our portfolio companies. In general, it can be said that there is subdued optimism. The higher taxes have been absorbed in earnings, and there is a certain recovery in economic activity (e.g. in construction), but there is caution as to how much the consumer can increase their consumption in the near term (a nurse today earns almost 30% less in real income compared to before the crisis). Interest rates remain relatively high even though inflation has come down significantly (9% policy rate compared to an inflation rate of about 1% and the central bank’s inflation target of 5%). Somewhat surprising was that none of the banks we met expected further significant reductions in the policy rate in the near term. Here we anticipate a unanimous caution against showing too much optimism until an agreement has been reached with the consortium in the negotiations on the Eurobond debts (if things go too well, the negotiations will be more difficult). At the meeting with Windforce, Sri Lanka’s leading player in renewable energy, we also got a clear example of the economic reforms through the IMF agreement starting to work. With the abandonment of fuel and electricity subsidies last year, the company has now recovered all previously withheld claims from the state-owned electricity transmission and distribution company (Ceylon Electricity Board) and can start looking ahead to new investments.

On the trip, we also had the opportunity to visit, among other things, Colombo’s future tourist magnet, City of Dreams Colombo. The project has been ongoing since 2014 but suffered delays due to the crises of the past 5 years. The first part of the hotel operations (Cinnamon Life) with just under 700 rooms is planned to open in the autumn and based on what we saw the timeline looked decently credible. The more important news, however, is the agreement that was concluded at the end of April with the international casino operator Melco, who will next year open an international casino in the complex, as well as run an exclusive hotel business (just over 100 rooms) on the top floors. Given Melco’s commitment and Colombo’s proximity to India, we believe the project can provide a good boost to tourism revenues in the years to come.

___________________________________

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you will be able to recover all of your investment. Historical return is no guarantee of future return. The Full Prospectus, KIID etc. are available on our homepage. You can also contact us to receive the documents free of charge. Please contact us if you require any further information: +46 8-5511 4570.