FUND PERFORMANCE – RENEWED FOCUS ON STRONG CORPORATE RESULTS

In USD the fund rose 6.6% during the month (EUR: 5.5%), compared to MSCI FMxGCC Net TR (USD) which rose 4.1% (EUR: +3.0%). In absolute terms, about 3.5% of the increase came from Vietnam, where our two largest holdings, the IT company FPT (+21%) and the bank Lien Viet Postal Bank (+39%), were the primary contributors. The second largest absolute return (+1.8%) came from Pakistan, where our largest holding Systems Ltd rose 15% and contributed around 1.3% in absolute return. Sri Lanka also made a positive contribution, mainly coming from our holding in Asiri Hospitals that rose 16% ahead of the quarterly report announcement. In January, we wrote about Asiri Hospitals’s strong earnings outlook for the next few years, and the quarterly numbers confirmed that our scenario still holds. The largest negative contribution in the portfolio came from Egypt (-0.4%), where our smaller position in Juhayna Foods (1.5% of the fund’s assets) fell by 20%. We described the problems in the company in our monthly letter for March. An added concern is that one of the company’s auditors requested more time to verify the financial statements for 2020, which delayed the company’s accounts and in the meantime created uncertainty in the market.

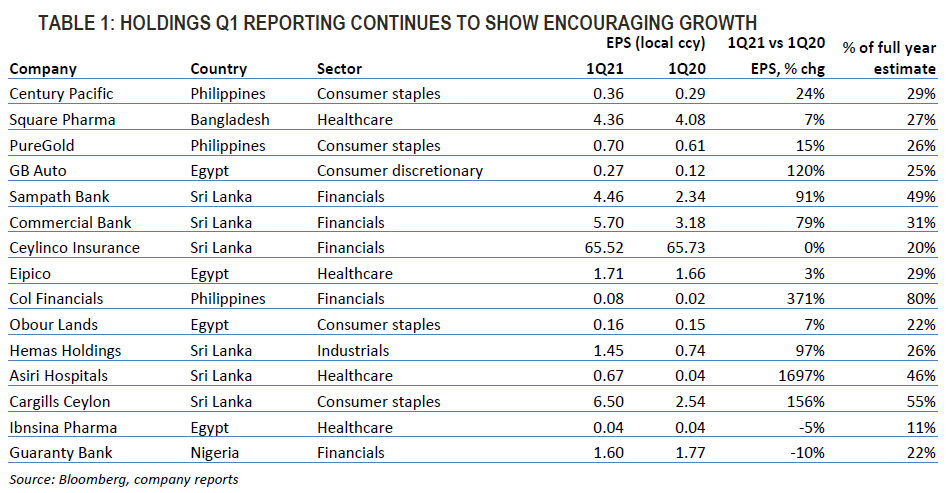

It was a relatively quiet month in our markets. Kazakhstan (+8%) and Pakistan (+6%) were the strongest performers, while Egypt (-6%) and Nigeria (-3%) showed the weakest development. The Covid-concerns that we described in last month’s letter gradually lessened with reduced number of infected which in turn means reduced risk of increased restrictions. Of our markets, only Sri Lanka and Vietnam (from very low levels should be added) saw a steady increase in the number of new cases throughout the month. Both countries showed very low number of cases until the most recent wave. Decreased concern for COVID-19 meant that we saw a delayed positive reaction to the strong company reports we described in last month’s letter. During the month, another 15 of our companies (37% of the fund’s assets) reported for the first quarter (calendar year) of 2021. The reports continued to come in slightly above expectations (see Table 1). The percentage increase on an annual basis is flattering given that the first quarter of 2020 was weak for most companies. But if we annualize the first quarter’s profit, however, we find that our companies delivered 29% of full-year expectations during the first quarter. With three quarters left, this indicates that profit estimates are likely to be raised slightly for the full year. With the fund’s valuation of 10.0x this year’s estimated profits, we remain optimistic.

CONCLUDING OUR ESG-ENGAGEMENT WITH ELSEWEDY

For the past nine months, we have been in dialogue with the portfolio company ElSewedy (Egypt) regarding their role as a contractor for the Rufiji Hydropower Project; a major dam project for hydropower in the Selous Game Reserve (World Heritage site, Tanzania). The project is deemed to violate Principle 7 under the Global Compact (“Support the precautionary principle regarding environmental risks”). Our engagement has included collaboration with non-governmental organizations in the environmental field, external sustainability consultants, and other experts. Tundra’s commitment has been focused on obtaining sufficient decision-making information and determining the extent to which we can alleviate negative effects from the project, especially regarding the environment, biodiversity, and endangered species. Tundra has also worked to ensure better access to information for the involved non-governmental organizations in the environmental field as well as the external sustainability consultants to base their assessment on. In accordance with our internal rule of 12 months’ engagement limit vis-à-vis companies that are deemed to violate international standards, we had until August 2021 to try to bring about a positive change. During May, however, we were forced to conclude that the respective restrictions of the parties involved would make it impossible to achieve a positive result within the timeline of our internal guidelines, and we have thus divested the holding. ElSewedy has spent considerable time discussing the project with us. Throughout the process, they have been cooperative and tried to meet the need for additional information. It is unfortunate that so many previous foreign shareholders in the company abandoned their shareholder role as soon as the problem was flagged. Together, we could probably have had a greater impact. We want to take this opportunity to reiterate that our door is always open to cooperation with other shareholders in our portfolio companies in the event of suspected norm-based violations. Together, our voice is stronger. A cut-and-run strategy achieves nothing.

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you will be able to recover all of your investment. Historical return is no guarantee of future return. The Full Prospectus, KIID etc. are available on our homepage. You can also contact us to receive the documents free of charge. Please contact us if you require any further information: +46 8-5511 4570.