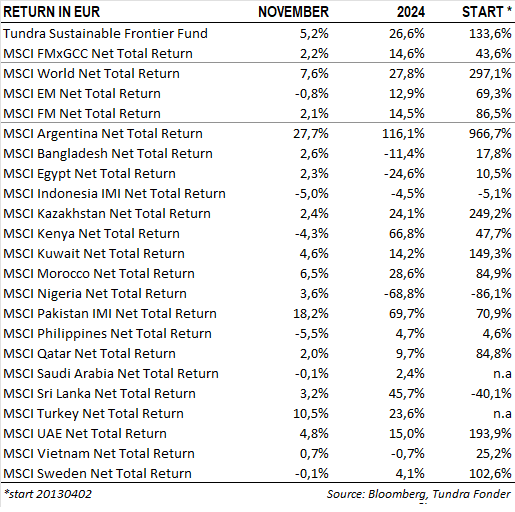

PAKISTAN LEADS THE WAY IN NOVEMBER

In November, the fund gained 2.3% in USD terms (EUR: +5.2%), outperforming the MSCI FMxGCC Net TR index, which declined by 0.7% in USD terms (EUR: +2.2%), and the MSCI EM Net TR index, which fell by 3.6% in USD terms (EUR: -0.8%). Positive contributors to the fund’s absolute return in USD included Pakistan (+2.7% portfolio contribution), Vietnam (+0.5%), and Sri Lanka (+0.3%), while the Philippines (-0.4%) was the weakest-performing sub-portfolio. Relative to the index, the strongest contributors were an overweight position in Pakistan (+2.1% relative contribution), no exposure to Romania (+1.1% relative contribution), and favorable stock selection in Vietnam (+1.1% relative contribution). On the downside, underperformance stemmed from stock selection and an underweight position in Morocco (-0.5% relative contribution), an overweight position in the Philippines (-0.4%), and the absence of holdings in Iceland (-0.4%). The fund’s largest single contributor was Pakistani IT company Systems Ltd, representing 8% of the portfolio, which rose by 13% following a strong quarterly report in the previous month. The second-largest contributor was National Bank of Pakistan (5% of the portfolio), which gained 18%, partly due to the removal of minimum deposit rate requirements for certain deposit categories. The largest negative impact came from Vietnamese consumer conglomerate Mobile World, which declined nearly 12% after a strong recovery earlier in the year.

PORTFOLIO ADJUSTMENTS

During November, the fund exited its position in Mobile World due to its strong recovery over the past two years and relatively high valuation, reallocating capital to better opportunities. Similarly, the fund divested Turkish software firm LOGO as the company’s performance failed to meet our expectations. Proceeds were partially reinvested in Vietnamese port operator Gemadept and Pakistani mobile assembler and distributor Airlink, expanding positions in promising sectors.

KEY MARKET EVENTS

Pakistan’s equity market rose by 15% in November, bringing year-to-date returns to 62%. The rally was fueled by domestic institutional investors returning to equities after sharp declines in interest rates. Inflation reached a six-year low of 4.9% year-on-year in November, prompting expectations of a 200-basis-point rate cut by the central bank in December. The central bank also revised its minimum deposit rate (MDR) policy, removing MDR requirements for institutional and corporate deposits while introducing a minimum profit-sharing rate for individual savings deposits in Islamic banks. This change is expected to compress Islamic banks’ net interest margins but benefit conventional banks, like National Bank of Pakistan. This regulatory change could increase National Bank of Pakistan’s earnings by 15% next year, while the fund’s only holding in an Islamic bank, Meezan Bank, next year’s earnings may see a negative impact of 8%.

November saw Sri Lanka’s Central Bank reduce its policy rate to 8.0%, transitioning to a single policy rate system. This was accompanied by deflationary pressures, with November’s CPI at -2.1%. Inflation is expected to turn positive by Q2 2025 and converge toward a medium-term target of 5%. Sri Lanka also launched its debt exchange program, targeting approximately USD 12.5 billion in International Sovereign Bonds (ISBs), with a deadline for bondholders set for December 12, 2024. Despite these developments, the stock market, which has gained 28% since mid-September, showed little reaction in November. In political developments, the ruling party, NPP, secured a two-thirds parliamentary majority, exceeding expectations. While this provides the government with a mandate for reforms, its coalition of 21 diverse political entities will need to maintain cohesion to ensure stability and effective governance.

HOW DO FRONTIER MARKETS RESPOND TO THE AMERICAN ELECTION?

Frontier markets responded cautiously to the U.S. presidential election. President Trump’s protectionist rhetoric has initially impacted the country’s major trading partners, with China as the primary target. Several companies we regularly engage within Pakistan, as well as insights from discussions during our recent trip to India, have highlighted significant export opportunities. These opportunities stem from Western companies’ ambitions to replace as many Chinese imports as possible with goods from other countries. US rhetoric remains aggressive, as evidenced by the outcomes of recent outbursts towards Mexico and Canada. However, predicting actual policy action—such as the Trump administration imposing shockingly high tariffs on all trading partners—is more complex. From an economic perspective, the U.S. cannot realistically do without the cheap imports that sustain its economy. Additionally, any countermeasures would severely impact American companies with global operations. On this point, most analysts seem to agree. However, analysts are divided into two camps regarding potential actions. One camp expects the administration to act recklessly, risking a full-scale trade war. The other believes the harsh rhetoric serves primarily as a negotiating tactic to benefit American businesses and the economy. U.S. stock markets appear aligned with the latter perspective, and we share that view.

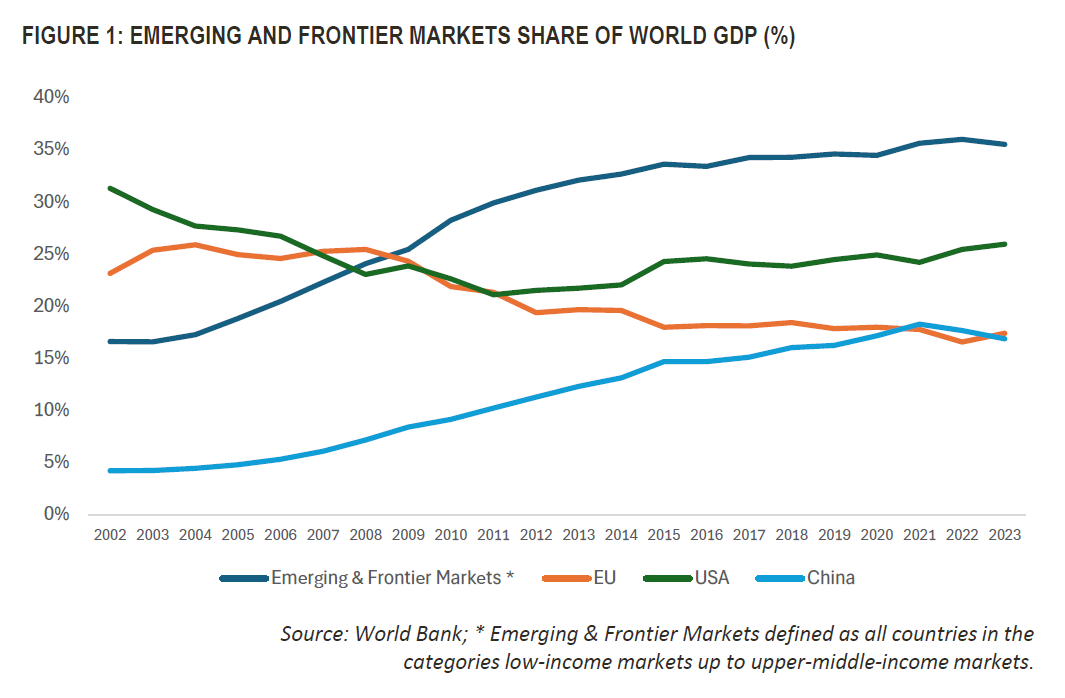

As investors, we adhere to Occam’s razor—the simplest explanation is often correct. Based on this principle, we conclude that the most rational strategy for the U.S. involves slowing the rise of China and other major developing countries as global leaders while maintaining access to imports and fostering relationships with growing export markets. Furthermore, Trump’s antagonistic approach—criticizing allies like Canada and Europe while promising reduced military involvement abroad—might inadvertently weaken what was once a united opposition to China. Emerging and frontier markets, comprising low-income to upper-middle-income countries as defined by the World Bank, are unlikely to take sides. Instead, they will act in their interests. India’s sharp increase in oil imports from Russia following the invasion of Ukraine exemplifies this pragmatism. Many of these countries maintain a cautious stance toward the U.S. and will not jeopardize relationships with other key trading partners.

Looking ahead to the next decades, it is inevitable that the fastest-growing segment of the global economy will continue to be emerging and frontier markets. Their influence will rise as America’s relative dominance diminishes. These countries are aware of this trajectory and are prepared to adopt a long-term perspective. The question remains how rationally the U.S. will act. While the rhetoric is likely to remain harsh and threatening, we hope the Trump administration’s economic understanding exceeds what is often expressed publicly, and that common sense will ultimately prevail. Regardless of the chosen path, we believe our primary markets—low-income and lower-middle-income countries—will continue to perform relatively well. Their rise is inevitable.

___________________________________

DISCLAIMER: DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you be able to recover all of your investment. Historical return is no guarantee of future return. The state of the origin of the Fund is Sweden. This document may only be distributed in or from Switzerland to qualified investors within the meaning of Art. 10 Para. 3,3bis and 3ter CISA. The representative in Switzerland is OpenFunds Investment Services AG, Seefeldstrasse 35, 8008 Zurich, whilst the Paying Agent is Società Bancaria Ticinese SA, Piazza Collegiata 3, 6501 Bellinzona, Switzerland. The Basic documents of the fund as well as the annual report may be obtained free of charge at the registered office of the Swiss Representative.