EGYPT AND VIETNAM LEAD THE WAY

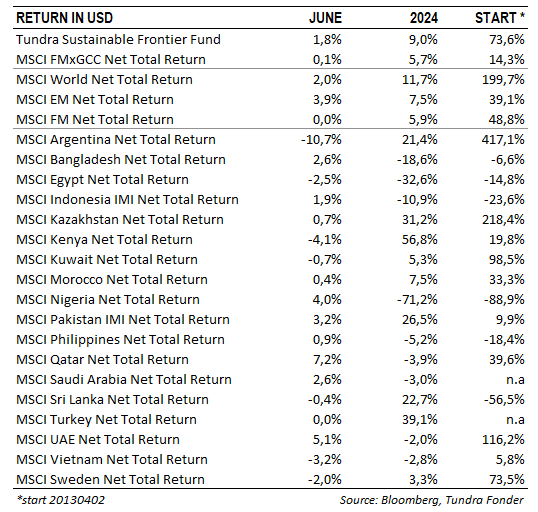

In USD, the fund rose 1.8% (EUR: +3.4%) during the month of June compared to the MSCI FMxGCC Net TR (USD), which rose 0.1% (EUR: +1.7%), and the MSCI EM Net TR (USD), which rose 3.9% (EUR: +5.6%). From an absolute return perspective, it was primarily Vietnam (+2.9% portfolio contribution) and Egypt (+1.2% portfolio contribution) that contributed positively. In comparison, it was mainly Pakistan (-1.5% portfolio contribution) and the Philippines (-0.8% portfolio contribution) which reduced the absolute return. For the third month in a row, it was primarily Vietnam contributing to the relative return versus the benchmark during the month. In USD our sub-portfolio rose 7%, compared to the market, which fell 3%.

KEY PORTFOLIO MOVES

The single biggest contribution came from the fund’s largest position, Vietnamese FPT Corp (9% of the portfolio), which rose 12%. The company reports financial data monthly. During the first five months of the year, turnover rose by 20% and profit after tax by 21%. Among individual holdings, the Egyptian GB Corp (5% of the portfolio) also stood out. The stock rose 24%, despite Egypt falling back slightly. During the month, there were rumors that the EBRD was about to buy into the company’s fintech company, MNT Halan, at an unexpectedly high valuation. The third biggest contribution came from Vietnamese airport operator, Airports Corporation of Vietnam, which rose 18% on continued positive momentum following the previous month’s strong passenger traffic figures. The biggest negative contributor was Philippine Century Pacific Foods (4% of the portfolio), which fell 14% without any specific news. The stock had a strong start to the year despite the generally weak performance of the Philippines, but since the end of March, it has fallen back on profit-taking. The second largest negative contribution came from the Pakistani textile company Interloop (4% of the fund), which fell 14% after the presentation of a new tax proposal, where exporters, such as Interloop, will lose their current preferential taxation. The tax news was somewhat mitigated by the company announcing its commitment to pursue an aggressive expansion plan, further strengthening the case of becoming the leading sustainable RMG (Ready Made Garment) exporter from Pakistan.

KEY MARKET NEWS

We had some key news during the month. Pakistan lowered the policy rate by 150 basis points (to 20,5%). With the latest inflation number for June at 12,6%, the real interest rate remains high and more cuts are likely to come during the year. At the time of writing (July 3rd), Sri Lanka has finally announced coming to an agreement with international bondholders regarding its defaulted Eurobond debt and now looks to exit the list of defaulting countries. Although it is a positive, and the timing was less than certain, it was also a widely expected event. With the negotiations out of the way, the investors’ focus will tilt more toward this autumn’s presidential elections, which remains uncertain. During the month, the IMF agreed to release the third installment of USD 1.14bn (out of a total of USD 4.7bn) to Bangladesh. As opposed to Sri Lanka and Pakistan, Bangladesh never saw the crisis headlines of its South Asian peers and has been going through a slower crisis-handling process, and is not out of the woods yet. We are likely to see more interest rate hikes and probably more currency weakening before it can overcome economic difficulties. On the other hand, the equity market’s valuation is now 2 standard deviations below its 10-year historical mean on P/BV, which indicates a lot is already priced in. Just as has been the case with Sri Lanka and Pakistan equities, markets tend to improve before headlines again turn positive.

PORTFOLIO COMPANIES’ PERFORMANCE

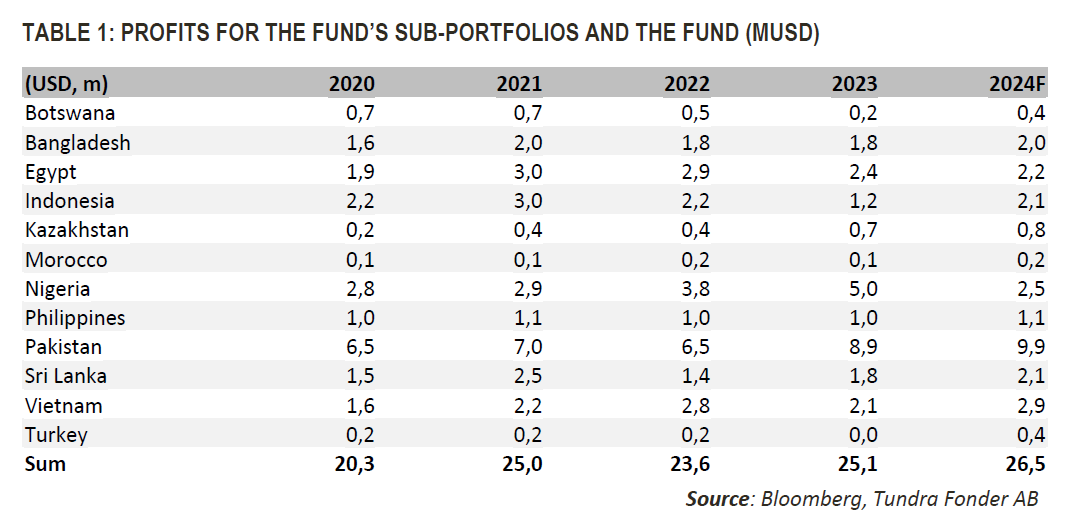

In our quarterly review of the portfolio companies’ profit development, we note some movements compared to the last review as of the end of March. The results of the Nigerian banks for the fourth quarter of 2023 were not published at the last review. These significantly exceeded expectations, primarily due to unexpectedly high revaluation gains and trading income (one-offs), which saw portfolio profits in Nigeria revised upwards significantly, from USD 2.8m to 5.0m. That meant the portfolio companies’ 2023 earnings rose 6% in 2023, compared to an expected 3% at the end of March. However, the upward adjustment of the Nigerian profits meant an increase in the base for 2023, which in turn means that the profit growth for 2024 has been revised down to 5% (against an expected 8% at the end of March). If we adjust for 2023, and instead compare the expected profits in 2024 with 2022, we note a marginal upward adjustment, from 11% profit growth to 12%. Among individual countries, we note that estimates in Sri Lanka for 2024 have been adjusted downward, from expected profit growth of 30% to 19%. We see this primarily caused by the higher tax levels in the wake of the IMF agreement. Positive to note is some upward adjustment in Vietnam, from 28% to 38% profit growth for 2024. We also note that investors have become somewhat more optimistic about Egypt. The previously expected drop in profit because of the devaluation has been reduced from -26% to -6% for 2024. In Pakistan, we note a smaller downward adjustment for 2024, from 19% to 11%. About half (5%) is due to the base for 2023 being adjusted upwards. However, with the last published results, we also note some downward adjustments in the IT sector (Systems Ltd in our case) and smaller adjustments in the banking sector, mainly due to expectations of interest rate cuts that have begun to take hold.

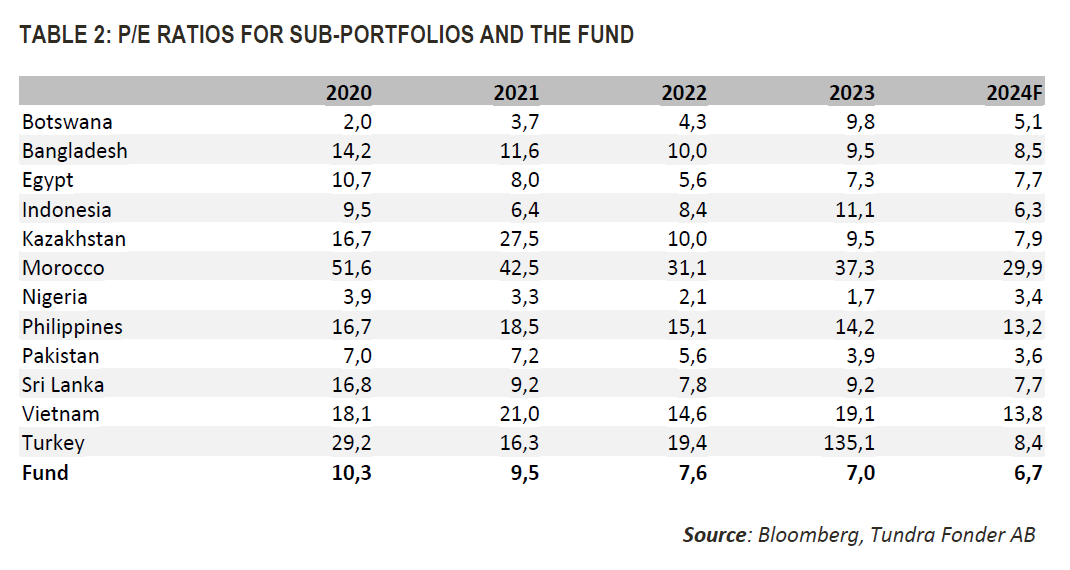

Looking at the valuation of the fund, we note that it is valued at 7.0x on 2023 earnings and 6.7x on expected earnings for 2024. This compares to the same portfolio’s valuation at the end of 2020 of 10.3x and at the end of 2021 at 9.5x. The fund thus would need to rise 36-54% to reach similar valuations as in 2020 and 2021, respectively. 2024 has started better for the fund, with a 9% (USD) rise so far. However, we note that investor concerns from the crises of recent years continue to weigh on valuations. This indicates that we are still early in a recovery phase, which makes us optimistic about better conditions ahead relative to more developed equity markets.

___________________________________

DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you be able to recover all of your investment. Historical return is no guarantee of future return. The state of the origin of the Fund is Sweden. This document may only be distributed in or from Switzerland to qualified investors within the meaning of Art. 10 Para. 3,3bis and 3ter CISA. The representative in Switzerland is OpenFunds Investment Services AG, Seefeldstrasse 35, 8008 Zurich, whilst the Paying Agent is Società Bancaria Ticinese SA, Piazza Collegiata 3, 6501 Bellinzona, Switzerland. The Basic documents of the fund as well as the annual report may be obtained free of charge at the registered office of the Swiss Representative.