CONTINUED CONSOLIDATION IN FEBRUARY

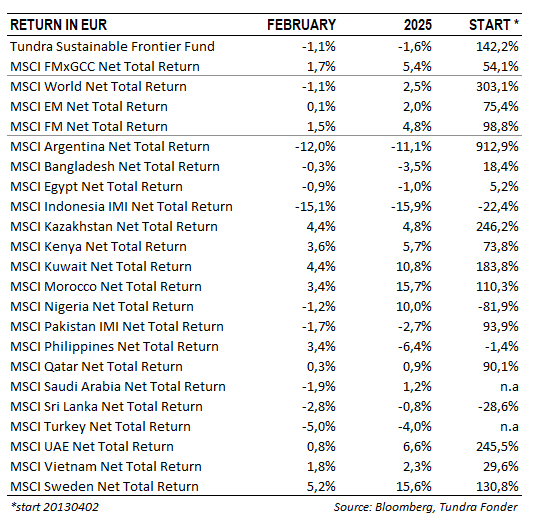

The consolidation we saw in January continued into February. In USD the fund fell by 0.8% (EUR: -1.1%) compared to the MSCI FMxGCC Net TR (USD), which rose by 2.0% (EUR: +1.7%), and the MSCI EM Net TR (USD), which rose by 0.5% (EUR: +0.1%). In absolute returns, the Philippines (+0.7% portfolio contribution), Sri Lanka (+0.3%), and Kazakhstan (+0.3%), were the positive contributors, while Vietnam (-0.7%), Pakistan (-0.4%), and Indonesia (-0.4%) were the markets that contributed most negatively. Relative to the benchmark, it was primarily our overweight position in the Philippines (+0.7% portfolio contribution relative to the benchmark), and our stock selection in Sri Lanka (+0.4%) that contributed positively to the relative performance. While our stock selection in Vietnam (-1.3%), underweight in Morocco (-0.7%), overweight in Indonesia (-0.4%), and absence of holdings in Romania and Slovenia (-0.4% each), contributed most negatively.

The largest individual contribution came from Vietnamese REE Corp (an industrial conglomerate with a strong focus on renewable energy) (7% of the portfolio), which rose by 11% in a stagnant stock market after being upgraded by one of the largest local brokerage houses. The second largest individual contribution came from Pakistani National Bank of Pakistan (6% of the portfolio). The stock rose by 13% ahead of its quarterly report. The report was released on March 3rd, and the company announced its first dividend since 2017 (for the fiscal year 2016). The largest negative contribution came from Pakistani Systems Ltd (8% of the portfolio), which fell by 9% during the month without any company-specific news. The second largest negative contribution came from Vietnamese IT company FPT (6% of the fund), which fell by 10% after its quarterly report. The report was in line with expectations, and the decline should perhaps be seen in the context that the stock rose 90% in 2024.

IMPRESSIONS FROM OUR TRAVELS IN FEBRUARY

In February, we undertook two trips. One was to Sri Lanka, where we met companies from Bangladesh, Sri Lanka, and Pakistan, and the other was to Vietnam, where we attended the country’s largest annual investor conference.

OBSERVATIONS FROM SRI LANKA

From our trip to Sri Lanka’s capital, Colombo, we made some general observations. The conference was much more well-attended this year (26 foreign investors, which was double the number from last year). The strong market performance of both Sri Lanka and Pakistan during 2024 was likely the reason. However, we note that even though interest has increased, it is still far from the conferences held ten years ago when around a hundred participants attended. At the conference, we had the opportunity to meet several of our portfolio companies, but also companies that play important societal roles, even though we are not shareholders.

For Sri Lanka as a country, we note that stability has now taken hold. Growth forecasts have been adjusted slightly upwards, while inflation remains low. In the recently presented budget, GDP is expected to grow by 5%, compared to the IMF’s forecast of 3.5%. The country is now gradually easing some import restrictions (which should neutralise the current account balance, which has been positive for a while), and inflation is expected to rise from the current level of -4% to the long-term target of 5% over the year. Tourism has now returned to the levels of late 2018 (before the Easter attacks in 2019) but has significant room to grow, provided that infrastructure investments keep up. A likely short-term measure is to build a temporary extra terminal at Colombo’s international airport. Especially for passengers arriving late in the evening, it is already very congested. According to leading industrial conglomerate John Keells, whom we met, such an expansion should be feasible within 8-12 months at a cost of less than USD 30 million and should enable Sri Lanka to receive approximately 4 million tourists per year (currently at around 2.5 million annually). This seems like a sensible investment, one that the new president, Dissanayake, also appears to support. The stock market has priced in stability with significantly higher stock prices. However, we would like to highlight that Sri Lanka’s geographical location near India and its strong potential in the services sector (particularly the tourism industry) has had a unique standing relative to other frontier markets, with valuations periodically in line with India. Provided that politicians make reasonably sound decisions moving forward, and that the recovery in the tourism industry is not interrupted, Sri Lanka may face a period of stable service-driven growth and reclaim its position as one of the ‘low-risk markets’ within the frontier category. Investors’ risk premium may therefore be significantly lower than is often the case with frontier markets, and valuations could increase further.

From our Pakistani meetings, we made some interesting observations. For us who have followed Pakistan since 2005, perhaps the most interesting observation was that the giant copper and gold project, Reko Diq, seems to have a good chance of going ahead. With strong support (and protection) from the military, it appears that the last obstacles may be cleared. If that happens, production should start (Phase 1) towards the end of 2028. Reko Diq is planned to be developed in several phases, with full production expected by 2034, at which point it will account for approximately 2% of global copper production and 0.5% of global gold production. Reko Diq has been discussed ‘seriously’ for two decades, and anyone who has followed Pakistan for a long time will, for good reasons, express some doubts before considering the potential positive effects for the country. The signal value of Pakistan moving forward would therefore be strong. Another potential milestone, where we also got the feeling that it could happen, was the privatisation of Pakistan International Airlines, a company that has completely stagnated since it helped Emirates get their airline started in 1985. We spoke with an industry player who is considering participating and who argued that the previously insurmountable issue of layoffs no longer seems to be a problem and that the landing rights PIA holds will likely make the company sufficiently attractive to end up in private hands. There were around ten Pakistani companies represented at the conference (more than from Sri Lanka, in fact). From our portfolio companies, we had the opportunity to meet Systems Ltd, Meezan Bank, AGP, and Airlink. All the companies performed well. AGP and Airlink are relatively new acquaintances for many foreigners and should be able to attract some new investors going forward.

In Bangladesh, one can notice that it is a market that has been off the radar of investors in recent years. During the previous government, transparency was low, with limited access (and low reliability) to official data, an ongoing but unmanaged crisis in the banking sector, and the capital market was often subject to whimsical temporary actions such as price floors (regulated price floors for individual stocks). The interim government has implemented significant changes, and we can see clear improvements in both transparency and crisis management. Although their lack of experience with government work was raised as a negative factor, we sensed a budding optimism among companies. By mid-year, the country is expected to have brought inflation under control, and we may start seeing interest rate cuts (one of the banks claimed that this could happen as early as spring). Of the countries represented at the conference, Bangladesh is probably the one that could see the largest increase in interest, from very low levels however.

IMPRESSIONS FROM VIETNAM

Vietnam’s largest conference, hosted by VietCapital, begins at the end of February and runs through the beginning of March in Ho Chi Minh City. Tundra usually participates, as it not only offers the opportunity to schedule many meetings in a concentrated format but also serves as a great way to gauge the sentiment of foreign investors. This year’s conference set a record for the number of participants (550). However, our impression was that the number of foreign participants was fewer than in previous years, with a very clear overrepresentation of local investors. We normally see this as a good sign, as it suggests that the stock market is not overheated. Vietnam is now an established market among emerging market investors and it is, of course, difficult to present exciting new companies every year. Both we, and colleagues from other frontier funds, noted that the representation of companies was somewhat thinner than usual, and we believe that the presentations made did not significantly alter existing investors’ views. Among the company meetings, we met with Vingroup, which was Vietnam’s largest company five years ago, whose persistent push for electric vehicles continues to confuse investors. Strong subsidies and unorthodox methods, such as starting its own ride hailing service (similar to Uber) and a charging company, have boosted local sales to 80-90,000 vehicles (the total car market in Vietnam is around 400,000 vehicles per year). However, foreign sales remain minimal, and it certainly doesn’t get easier with the growing competition from Chinese car manufacturers (most recently Xiaomi). We must give the company credit for its design and innovative thinking. For example, we really liked their new mini-SUV VF3. However, we still find it hard to see value for Vingroup’s shareholders. The market value is now down to around USD 6 billion (from a peak of USD 21 billion in April 2021), and an additional (at least) USD 750 million in financing commitments exists, including a new assembly plant in Indonesia, which is overshadowing their other businesses. The upside for shareholders (we are not one of them) likely lies in a takeover by someone who wants to buy into the Vietnamese market and/or sees value in the high-tech production capacity that has been built up (around 300,000 vehicles per year at present).

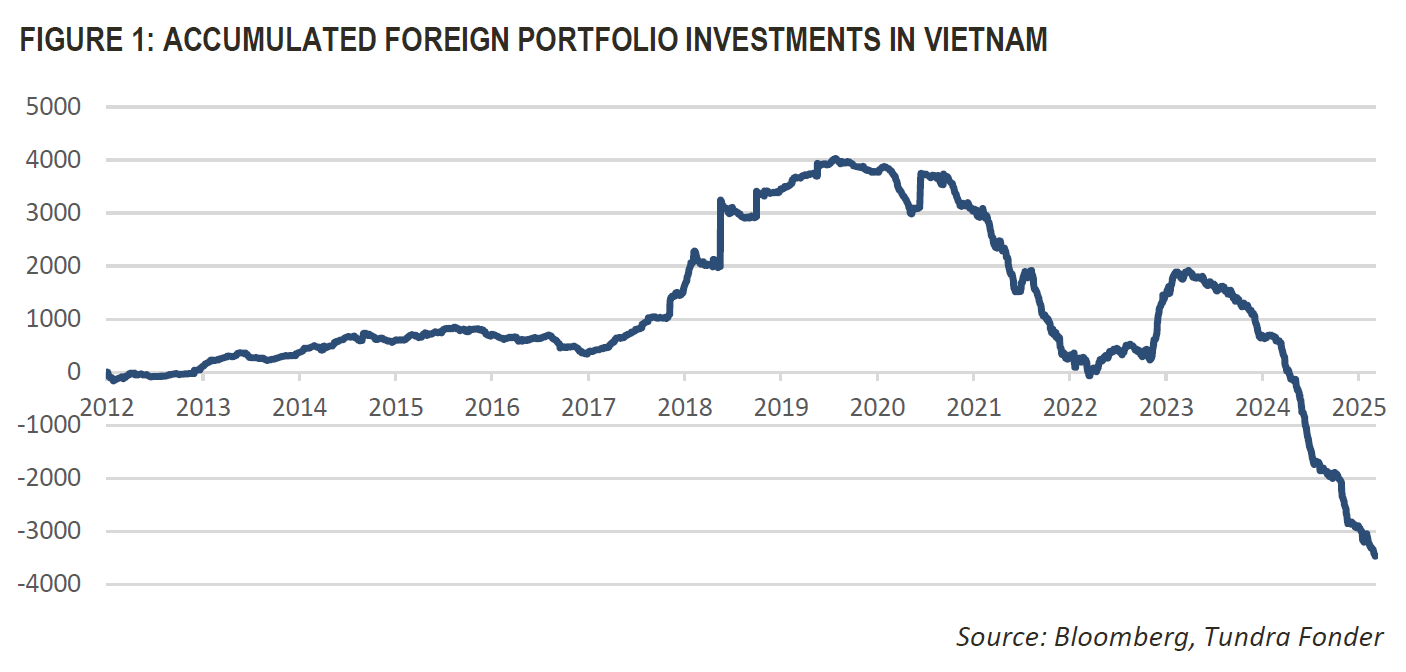

Vietnam has been in a somewhat unusual situation in recent years. Until the end of 2021, the stock market was a favourite among foreign investors. Not only was it an important market for frontier investors, but we also saw significant flows from emerging market funds as turnover rose to nearly USD 1 billion per day, and we also saw large flows into Vietnam funds from neighbouring countries’ investors (e.g. South Korea). From 2022 onwards, the flow reversed, and the stock market has underperformed both frontier and emerging market indices.

One of the more interesting presentations at the conference was given by a representative from the Central Party Committee for Strategic Planning. This confirmed our previous thesis (see the September 2023 monthly letter) where we argue that the large presence of foreign companies operating in Vietnam has caused capital to be repatriated to place in US Treasury bonds post the rate hikes in the US. This has put pressure on the Vietnamese Dong and meant that the central bank in Vietnam has had to keep interest rates higher than what could be justified by inflation levels and consumer demand. The representative confirmed Vietnam’s sensitivity to the actions of the Federal Reserve in the short term. The presentation also provided an interesting insight into how Vietnam benchmarks itself against other countries that have made the transition from low-income to high-income countries. Vietnam primarily benchmarks itself to China, South Korea, Singapore, and Taiwan, and tries to draw lessons from their historic development. The presentation also gave a glimpse of future priorities, where investments in digital infrastructure (the digitisation of the economy to achieve productivity improvements) appear to be an important area for the period 2026-2030.

During our days in Saigon (the other name for Ho Chi Minh City), we had the opportunity to test the new subway. The first line, out of currently four planned, was inaugurated in December 2024. The nearly 20 kilometers stretch resembles Singapore’s similar lines, including shields at the platform that prevent movement onto the tracks. The expansion will, like in Singapore, be an important support to relieve the pressure on Saigon’s traffic-heavy streets.

___________________________________

DISCLAIMER: DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you be able to recover all of your investment. Historical return is no guarantee of future return. The state of the origin of the Fund is Sweden. This document may only be distributed in or from Switzerland to qualified investors within the meaning of Art. 10 Para. 3,3bis and 3ter CISA. The representative in Switzerland is OpenFunds Investment Services AG, Seefeldstrasse 35, 8008 Zurich, whilst the Paying Agent is Società Bancaria Ticinese SA, Piazza Collegiata 3, 6501 Bellinzona, Switzerland. The Basic documents of the fund as well as the annual report may be obtained free of charge at the registered office of the Swiss Representative.