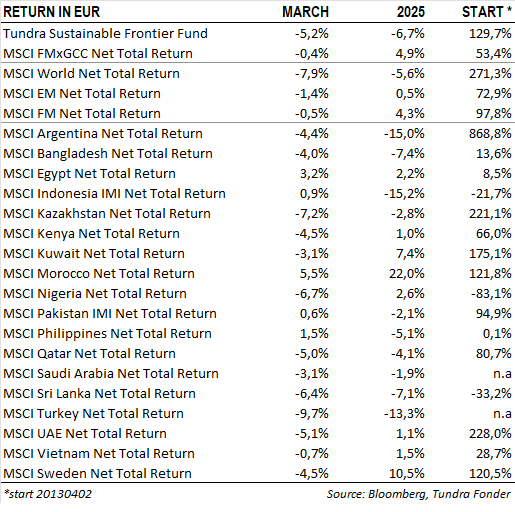

In USD the fund declined by 1.5% in March (EUR: -5.2%), compared with a 3.4% rise for the MSCI FMxGCC Net TR (USD) (EUR: -0.4%) and a 2.4% (EUR: -1.4%) rise for the MSCI EM Net TR (USD). In absolute terms, measured in USD, the largest positive contributions came from Pakistan (+0.7% contribution to absolute portfolio returns), and Egypt (+0.7%), while Vietnam (-1.4%), and Indonesia (-0.6%) were the main detractors.

Relative to the index, the main positive contributions came from our position in Egypt (+0.7% relative contribution), and our overweight in Pakistan (+0.4%). On the negative side, the key detractors were our stock selection in Vietnam (-1.9%), underweight position in Morocco (-1.4%), overweight in Indonesia (-0.7%), and underweight position in Romania (-0.5%).

On individual stock level our position in Egyptian fintech/industrial conglomerate GB Corp (6% of the portfolio) rose 20% after releasing better-than-expected full-year results. The second best contributor was Pakistani Meezan Bank (6% of the portfolio) which rose 5%, after a period of underperformance vs the general market. The largest negative contribution came from Vietnamese IT-company FPT Corp (5% of the portfolio) which fell 12% during the month. Vietnam continues to experience net foreign outflows, and FPT Corp is one of the most common holding among international investors. The second-largest detractor was Indonesian Hermina Hospitals (3% of the portfolio), which declined 23% following a Q4 report that showed slightly lower-than-expected margins (more on this below).

WHAT ARE THE MAIN REASONS FOR THE WEAK START TO THE YEAR?

Following a strong 2024, during which the fund rose 25% (USD)—16% ahead of its benchmark—2025 has begun on a weaker note relative to the index. In USD the fund is down 3% year-to-date, underperforming the benchmark by 12 percentage points. While our high active share means deviations from the index are to be expected, this is nonetheless an unusually large underperformance. We thus want to outline the key reasons behind it and share our thoughts on recent market developments:

• Sharp weakening of the US dollar – So far this year, the dollar has weakened by approximately 4% against the euro. About 45% of our benchmark, the MSCI FMxGCC Net TR (SEK), is composed of countries with currencies more closely tied to the euro than the dollar (e.g., Morocco 14%, Romania 12%, Slovenia 7%, Iceland 6%, Croatia 4%, Estonia 0.8%, Lithuania 0.8%). These countries have been among the best-performing markets in the benchmark this year. In contrast, our largest markets—Pakistan (26%), Vietnam (20%), Sri Lanka (11%), Egypt (10%), Bangladesh (9%), the Philippines (7%), and Indonesia (4%)— the currencies of these markets tend to be more closely aligned with the US dollar in the short term, as the dollar is the primary currency for FX trading. A weaker dollar typically leads to market rallies, driven both by improved competitiveness in export markets outside the US, by the fact that their foreign currency debts are primarily denominated in dollars, as well as by higher asset values on their balance sheets.

• Underweight in Morocco – Our underweight in Morocco (14% of the benchmark), where we only own payment solutions company HPS (2% of the fund), has hurt particularly hard in the beginning of the year. In USD the equity market is up 27% so far in 2025. Although Morocco has been a resilient outperformer on a top-down level, helped by its proximity to major European markets, we have a hard time finding value in the equity market. Supported by a significant local institutional investor base the general valuation of 20x earnings is too high in our view, especially as most larger companies are relatively mature businesses. A warning sign in terms of the local sentiment is the two largest cement companies which are trading at P/E 30x, and P/S of 5-6x. This is 4-5x higher than in most frontier markets. To be fair, the high valuation in Morocco is not a new phenomenon and we are the first to acknowledge that the macro and political stability the market has shown over the years are supportive of a premium. It is still not for us.

• Weak relative performance in our Vietnam sub-portfolio (20% of the fund) – Through the end of March, our Vietnam sub-portfolio declined by 10% (USD), while the Vietnamese market has risen by 6%. As noted in our January letter, Vietnam was the single largest positive contributor in 2024, with our holdings rising 49% compared to 5% decrease in the broader Vietnamese market. A portfolio that outperforms by over 50 percentage points in a year will, inevitably, underperform at times. This is a natural and expected fluctuation.

• Weak performance in the Philippines and Indonesia – Currently, we have approximately 11% of the fund allocated to these two markets (7% in the Philippines, 4% in Indonesia), both of which have come under pressure in recent months, especially the smaller companies where the fund is positioned. Our Philippines portfolio is down 9% year-to-date, and Indonesian portfolio 29%. Indonesia’s decline appears to be an overreaction to concerns about a slowing economy and discontent with the new president. The Indonesian rupiah has been Asia’s weakest currency this year, falling 6% against the dollar. The Philippines has faced its own political headlines, including the legal proceedings against former President Duterte, but its weakness is likely more a sympathy reaction to Indonesia’s underperformance, as they share a similar foreign investor base. Some moves have been extreme. As an example, our Indonesian healthcare holding, Hermina Hospitals, is down 29% so far this year. We met with the company at the ASEAN Conference in Bangkok in the beginning of March, and we left the meeting more positive than before. Hermina is now raising its growth ambitions on the back of strong demand from local doctors to open more hospital, as well as favourable reforms in Indonesia’s healthcare sector.

• Consolidation in Pakistan and Sri Lanka (27% and 11% of the portfolio) – Our Pakistan sub-portfolio rose 68% last year, while our Sri Lankan holdings gained 53%. Both markets are down slightly this year. Nevertheless, we see this as a consolidation phase with underlying strength. Despite substantial foreign outflows, local investors have stepped in to absorb selling pressure, and prices have held relatively firm. We view Sri Lanka as a relatively stable market going forward, with the potential to deliver acceptable returns at lower risk compared to most frontier markets. Pakistan remains the market where we expect another significant upward movement before transitioning into a phase where stock selection becomes the primary driver of returns.

To summarise the start of the year, we can conclude that all parts of the portfolio have moved against us in the short term, but the reasons for this are relatively easy to understand. We are currently facing a unique global situation, where factors other than developments in our countries and portfolio companies have been the dominant drivers. While this may continue to impact us in the short term, with a bit of perspective, it tends to present good buying opportunities.

TRUMP STARTS HIS CHICKEN RACE

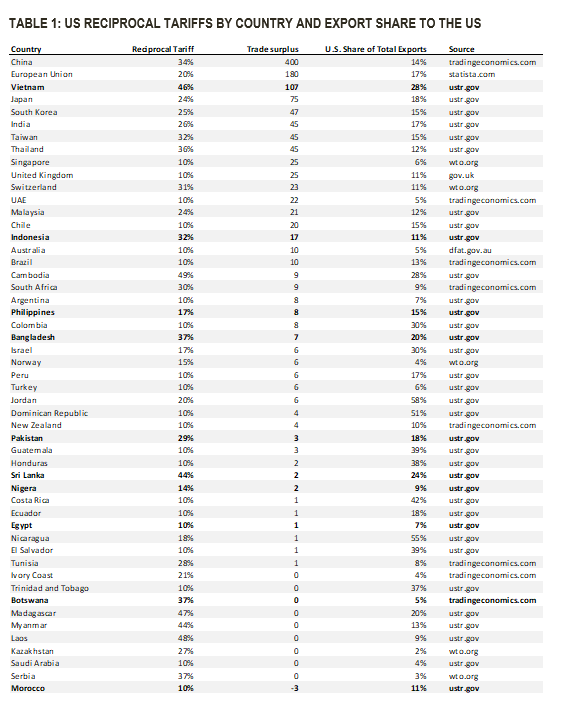

On Wednesday evening, April 2nd, Trump proudly announced his retaliatory tariffs, and the door is now open for negotiations until 9 April. As such, there is a significant risk that what we are writing here may soon become outdated, or at least by the time of the next monthly report. Based on a subjective calculation of how countries have disadvantaged the United States in their trade policies the United States has come up with what they refer to as reciprocal tariffs, the original proposal is outlined below. It is important to note that, in the case of China, the increase is in addition to the 20% tariff that was introduced just over a month ago. The table also includes an estimate of the most recent trade surplus figures, as well as the share of exports that go to the US. The countries in which Tundra invests on behalf of the fund are highlighted in bold. Sources are provided in the table.

Based on the original proposal, Vietnam is expected to be hit the hardest. Vietnam has an extremely high level of trade as a percentage of GDP, nearly 200%. From a trade balance perspective, it is important to note that Vietnam’s imports constitute nearly 95% of its exports, meaning the effect on the trade balance is less significant. However, should the proposal remain in place, it would initially have a severe impact on the country’s economy. Sri Lanka faces the next highest tariffs, but its trade with the US is currently relatively limited. Pakistan and Bangladesh both have large textile industries that will be affected by the tariffs. However, their main competitor remains China, which, including the previously announced 20% tariffs, will see its products become 54% more expensive. Higher import prices for American consumers should reduce demand, but people will still need to buy clothes. Egypt fares the best, as it is only affected by the standard 10% tariff.

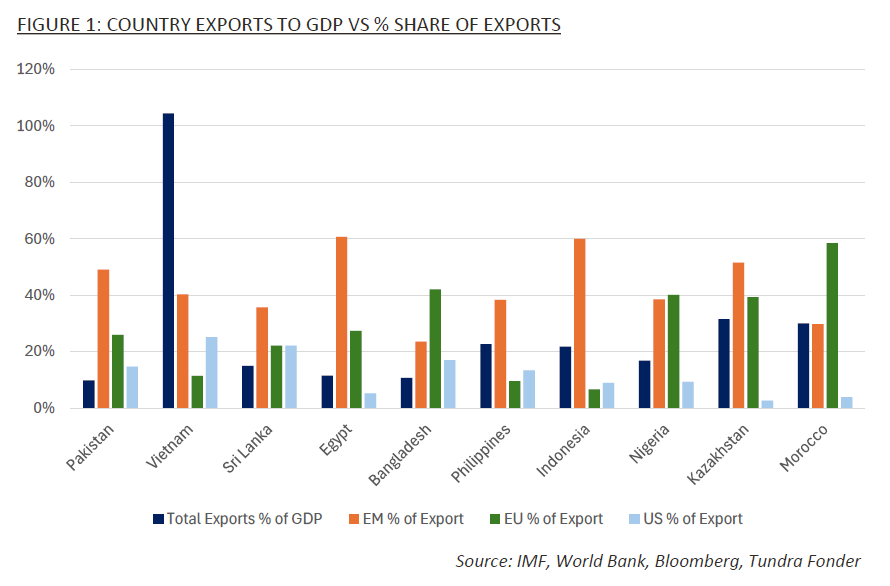

As mentioned, we expect significant changes relative to the proposal put forward on Wednesday evening, and it is premature to draw any long-term conclusions at this stage. We consider the risks to be greatest for the US economy, given the potential for delays, increased cost or the loss of access to critical goods for domestic consumption and production. A worst-case scenario, of course, is that this escalates into a full-scale trade war. We still believe the likelihood of this is very low, but we will have to live with uncertainty for a while longer. It is also important to remember that this is only impacting US trade vs the rest of the world, not the trade between other countries. As can be seen in the graph below, the intra-trade between emerging and frontier markets are significantly more important than their trade with the U.S.

___________________________________

DISCLAIMER: DISCLAIMER: Capital invested in a fund may either increase or decrease in value and it is not certain that you be able to recover all of your investment. Historical return is no guarantee of future return. The state of the origin of the Fund is Sweden. This document may only be distributed in or from Switzerland to qualified investors within the meaning of Art. 10 Para. 3,3bis and 3ter CISA. The representative in Switzerland is OpenFunds Investment Services AG, Seefeldstrasse 35, 8008 Zurich, whilst the Paying Agent is Società Bancaria Ticinese SA, Piazza Collegiata 3, 6501 Bellinzona, Switzerland. The Basic documents of the fund as well as the annual report may be obtained free of charge at the registered office of the Swiss Representative.